Retirement Savings Portability (3)

Consolidation Corner Blog

Consolidation Corner is the Retirement Clearinghouse (RCH) blog, and features the latest articles and bylines from our executives, addressing important retirement savings portability topics.

Refundable Saver’s Tax Credits Would Significantly Reduce Retirement Savings Shortfall—Especially for Minorities

Concurrent with the COVID-19 pandemic, our elected representatives have been grappling with the issue of wealth disparities between America’s white and minority workers. Commendably, there has been bipartisan support in Washington, DC for measures to assist those who are historically under-served or under-saved in our national system for accumulating and incubating retirement savings.

Concurrent with the COVID-19 pandemic, our elected representatives have been grappling with the issue of wealth disparities between America’s white and minority workers. Commendably, there has been bipartisan support in Washington, DC for measures to assist those who are historically under-served or under-saved in our national system for accumulating and incubating retirement savings.

Beware of Second Order Effects for Retirement Savings Public Policies

At first glance, some retirement savings public policies can seem like a sure thing, particularly when they’re based solely upon the benefits that would directly result. However, in the real world, these “first order” effects are inevitably followed by “second order” effects, which can sometimes be antithetical to the policy’s original intent.

At first glance, some retirement savings public policies can seem like a sure thing, particularly when they’re based solely upon the benefits that would directly result. However, in the real world, these “first order” effects are inevitably followed by “second order” effects, which can sometimes be antithetical to the policy’s original intent.

Don’t Relegate Lost & Missing Accounts to the Lost & Found—Consolidate Them in the Retirement System

The Securing a Strong Retirement Act of 2021, nicknamed the “SECURE (Setting Every Community Up for Retirement Enhancement) Act 2.0,” was passed unanimously by the House Ways and Means Committee, and many expect the bill to pass the full House of Representatives.

How Sponsors can Facilitate Better Participant Outcomes—and Improve Plan Metrics—in 2021

You don’t need me to remind you that 2020 has been an extraordinary year that many of us would like to forget. The New Year we have been looking forward to for some time is now here.

Elections Have Consequences—Elect to Help Participants Keep Their Savings, Instead of Losing Their Savings via Mandatory Distributions

No, this article isn’t about the Presidential election. But this year’s election, which took place in the middle of a global pandemic, reminds us that some things are in our control, and some things aren’t.

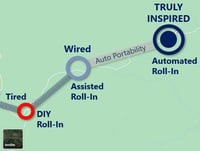

From Tired to Inspired: A Roadmap for 401(k) Roll-Ins

As I wrote in a previous article, 401(k) automated portability is an idea whose time has come. To achieve that vision, how will we get from the present state to full automation of the plan-to-plan roll-in process?

As I wrote in a previous article, 401(k) automated portability is an idea whose time has come. To achieve that vision, how will we get from the present state to full automation of the plan-to-plan roll-in process?

This article, as well as the video below, offers readers a roadmap for the progression from ‘tired’ to ‘wired’ and finally, to the ‘inspired’ state that will eventually characterize 401(k) roll-ins.

Every Dollar Counts in Today’s Zero-Interest-Rate Environment

It’s no secret that interest rates have been at historically low levels for quite some time, but the recent announcement by Federal Reserve Chairman Jerome Powell indicates that rates will stay near zero for the foreseeable future. Chairman Powell stated in his address last month that the Fed would tolerate above-2% inflation instead of attempting to preemptively control inflation by raising interest rates.

How to Mitigate COVID-19’s Potentially Catastrophic Impact on Americans’ Retirement Readiness

It’s bad enough that more than 50 million Americans have filed claims for unemployment benefits since the start of the COVID-19 pandemic and lockdown. But in addition to the disruption, financial hardship, and uncertainty that unemployed Americans (and their families) are experiencing right now, this crisis also threatens their financial security during retirement.

COVID-19 Pandemic Demonstrates the Need for Institutionalized Portability

The COVID-19 crisis has created a situation where tens of millions of American workers are in danger of seeing their retirement savings depleted. In addition to the awful death toll, the COVID-19 outbreak has led to extreme disruption in daily life, financial markets, and the economy—especially employment. As of May 28, more than 40 million Americans filed claims for unemployment benefits in the previous 10 weeks. This deadly combination of 1) levels of unemployment not seen since the Great Depression, 2) a significant market downturn, and 3) the ongoing plan-to-plan portability gap, has serious implications for these Americans’ retirement outcomes.

To Show Participants You Care, Help Them Avoid Cashing Out Post-CARES Act

It goes without saying that we are not living in normal times. The health and safety of our families and communities are paramount, and measures to ease burdens and hardships are always appreciated. These include the Coronavirus Aid, Relief, and Economic Security (CARES) Act, the massive fiscal stimulus signed into law on March 27, 2020.