401k Consolidation (6)

Consolidation Corner Blog

Consolidation Corner is the Retirement Clearinghouse (RCH) blog, and features the latest articles and bylines from our executives, addressing important retirement savings portability topics.

Assessing the State of DC Plans & Retirement Savings, 15 Years After the Pension Protection Act

Traditionally, the anniversary gift for couples celebrating their 15th wedding anniversary is crystal. When the Pension Protection Act of 2006 was signed into law 15 years ago, a crystal ball would have been useful. Although this legislation was (commendably) crafted with the best of intentions, its unintended consequences for defined contribution plan participants and sponsors continue to reverberate.

Traditionally, the anniversary gift for couples celebrating their 15th wedding anniversary is crystal. When the Pension Protection Act of 2006 was signed into law 15 years ago, a crystal ball would have been useful. Although this legislation was (commendably) crafted with the best of intentions, its unintended consequences for defined contribution plan participants and sponsors continue to reverberate.

Refundable Saver’s Tax Credits Would Significantly Reduce Retirement Savings Shortfall—Especially for Minorities

Concurrent with the COVID-19 pandemic, our elected representatives have been grappling with the issue of wealth disparities between America’s white and minority workers. Commendably, there has been bipartisan support in Washington, DC for measures to assist those who are historically under-served or under-saved in our national system for accumulating and incubating retirement savings.

Beware of Second Order Effects for Retirement Savings Public Policies

At first glance, some retirement savings public policies can seem like a sure thing, particularly when they’re based solely upon the benefits that would directly result. However, in the real world, these “first order” effects are inevitably followed by “second order” effects, which can sometimes be antithetical to the policy’s original intent.

At first glance, some retirement savings public policies can seem like a sure thing, particularly when they’re based solely upon the benefits that would directly result. However, in the real world, these “first order” effects are inevitably followed by “second order” effects, which can sometimes be antithetical to the policy’s original intent.

Don’t Relegate Lost & Missing Accounts to the Lost & Found—Consolidate Them in the Retirement System

The Securing a Strong Retirement Act of 2021, nicknamed the “SECURE (Setting Every Community Up for Retirement Enhancement) Act 2.0,” was passed unanimously by the House Ways and Means Committee, and many expect the bill to pass the full House of Representatives.

Leakage and Auto Portability Featured at Senate HELP Committee Hearing

On May 13, 2021, the U.S. Senate’s Committee on Health, Education, Labor and Pensions (HELP) held its first hearing on retirement security since 2013. With testimony from a blue-ribbon panel of witnesses, the hearing had a broad focus, but the topic of retirement savings leakage, and its most-promising solution, auto portability, were prominently featured.

On May 13, 2021, the U.S. Senate’s Committee on Health, Education, Labor and Pensions (HELP) held its first hearing on retirement security since 2013. With testimony from a blue-ribbon panel of witnesses, the hearing had a broad focus, but the topic of retirement savings leakage, and its most-promising solution, auto portability, were prominently featured.

Auto Portability is an Easily Quantifiable Solution for Helping Participants Achieve Financial Wellness

Financial wellness has taken on a new urgency over the past year as we have witnessed a series of “once-in-a-lifetime” events that affect how we work and save for retirement. In response, many plan sponsors have adopted new and important tools to strengthen the financial wellbeing of their participants.

What’s Missing from Many Plans? Current Addresses for Participants

So many extraordinary developments took place last year that some trends fell under the radar. One of these—the sharp uptick in migration out of large U.S. cities—can make a significant impact on sponsors and their plans.

Auto Portability Is, And Always Will Be, A Bipartisan Solution

With Boston Mayor Marty Walsh’s nomination to become Secretary of Labor advancing through the Senate, the transfer of power in Washington, DC is progressing. Although the Department of Labor is taking direction from a Democratic administration, the solution to the problem of rampant asset-leakage from the U.S. retirement system will remain on track.

Nudge Theory can Help Sponsors Strengthen Financial Wellness Initiatives

After the year we’ve had, it’s no wonder there is so much more concern about financial wellness. But while plan sponsors are well-intentioned in their efforts to help participants increase their retirement savings and other financial outcomes, the latter haven’t noticed.

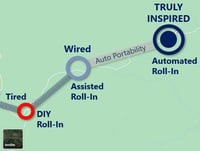

From Tired to Inspired: A Roadmap for 401(k) Roll-Ins

As I wrote in a previous article, 401(k) automated portability is an idea whose time has come. To achieve that vision, how will we get from the present state to full automation of the plan-to-plan roll-in process?

As I wrote in a previous article, 401(k) automated portability is an idea whose time has come. To achieve that vision, how will we get from the present state to full automation of the plan-to-plan roll-in process?

This article, as well as the video below, offers readers a roadmap for the progression from ‘tired’ to ‘wired’ and finally, to the ‘inspired’ state that will eventually characterize 401(k) roll-ins.