Much has been written about America’s retirement-savings shortfall. Much has also been written about one of the major reasons for this shortfall—the lack of technology and operating standards to make seamless plan-to-plan savings portability easy for America’s highly mobile workforce. The cumbersome and costly nature of DIY portability has made prematurely cashing out small-balance 401(k) savings accounts, or stranding them in former employers’ plans, the easiest options for many participants after they change jobs.

Much has been written about America’s retirement-savings shortfall. Much has also been written about one of the major reasons for this shortfall—the lack of technology and operating standards to make seamless plan-to-plan savings portability easy for America’s highly mobile workforce. The cumbersome and costly nature of DIY portability has made prematurely cashing out small-balance 401(k) savings accounts, or stranding them in former employers’ plans, the easiest options for many participants after they change jobs.

The vast majority of leakage of 401(k) savings from the U.S. retirement system (89%, according to the Government Accountability Office) is the result of cash-outs. However, women and minorities have much higher cash-out rates than their male and white counterparts, respectively, making their retirement nest eggs far more susceptible to harm.

In the case of minority participants, data from the U.S. Census Bureau, Employee Benefit Research Institute (EBRI), and Ariel/Aon Hewitt indicates African-American plan participants are 61.5% more likely to cash out than non-minority participants, and that figure climbs to 134% for African-Americans with household incomes below $20,000 per year. High cash-out rates exacerbate an already challenging situation for minority retirement-savers—these same sources have found that African-American and Hispanic-American plan participants have a job turnover rate which is 28% higher than their non-minority counterparts, and on top of that, they are significantly underrepresented in the U.S. defined contribution plan system. Only 25% of plan participants are minorities, even though minorities constituted 39% of the U.S. population in 2015 and are projected to account for 56% of Americans by 2060.

Last month, Robert L. Johnson, founder of Black Entertainment Television (BET) and Chairman of Retirement Clearinghouse, called the nation’s attention to the high 401(k) cash-out rates among African-Americans saving for retirement. During his remarks at the White House, at the ceremony for the signing of the executive order which created the White House Opportunity and Revitalization Council on December 12, 2018, Mr. Johnson noted that 60% of African-Americans and Hispanic-Americans cash out their 401(k) accounts.

In his remarks at the White House and in subsequent media interviews, Mr. Johnson identified the solution to this acute problem for America’s minority communities—auto portability. He pointed out that this innovation (which first went live in July 2017), when combined with measures to increase coverage, would add close to $800 billion in retirement savings into the pockets of minority Americans if plan sponsors throughout the country adopt it.

The auto portability solution is underpinned by paired “locate” and “match” algorithms programmed to locate and confirm the identity of participants who have left small 401(k) accounts behind in former-employer plans or had their accounts forcibly rolled into safe harbor IRAs, and start the process of automatically rolling those assets into active accounts in their current-employer plans.

A Boston Research Group case study, focusing on a large plan sponsor in the healthcare services industry, has already demonstrated that sponsors can maximize the impact of auto portability if they implement it as a default process, which requires affirmative consent to opt out of the program instead of opting into it. The U.S. Department of Labor (DOL) understands and appreciates this, and has introduced legal guidelines to make the widespread adoption of auto portability a reality. The DOL’s recent guidance on auto portability, issued in the form of an Advisory Opinion and a proposed Prohibited Transaction Exemption clarifying fiduciary liability for sponsors when they add auto portability as a default process, clears the path toward the broad adoption of auto portability.

Momentum Leads to Optimistic Outlook for the 401(k)’s Next 40 Years

The progress on the auto portability front is highly promising for all plan participants, and especially for minority participants, because it coincides with efforts in Washington to promote increased coverage by expanding the reach of multiple-employer plans.

According to a scenario under our Auto Portability Simulation (APS), in which we assume open multiple-employer plans add 16.7 million active participants from small and medium-sized businesses to the U.S. defined contribution system, overall minority participation would increase from 16.4 million participants today to 52.7 million participants in 2058. Specifically, the amount of African-American participants in defined contribution plans would rise from 6.6 million participants today to 14.2 million participants in 2058.

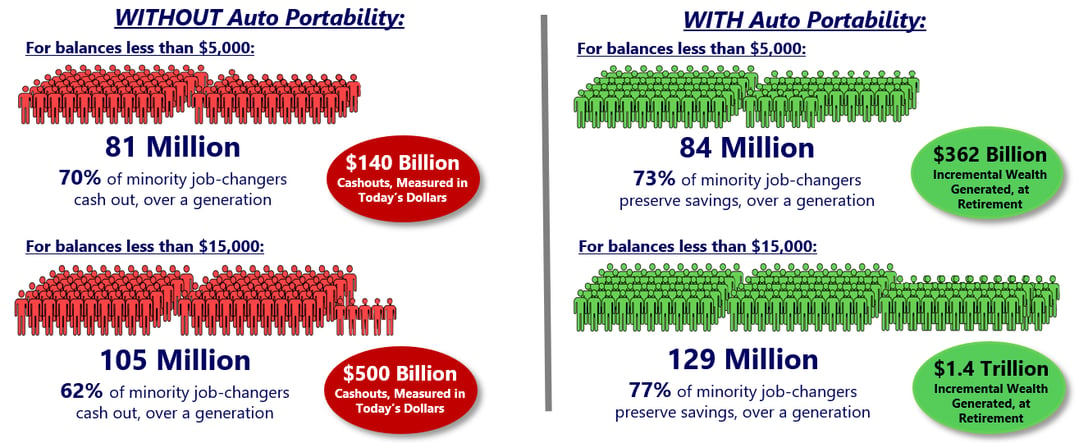

If auto portability is also widely implemented (see Figure 1) under this 40-year scenario, 84 million minority participants—or 73% of minority job-changers with 401(k) balances of less than $5,000—would preserve and accumulate $362 billion in retirement savings. If the auto portability threshold is increased to allow for the automatic portability of 401(k) accounts with less than $15,000, then 129 million minority participants would preserve $1.4 trillion in retirement savings over the next 40 years.

However, without auto portability, minority job-changers with 401(k) balances of under $5,000 would cash out $140 billion in today’s dollars over the 40-year timeframe. When the auto portability threshold is raised to $15,000 under this scenario where auto portability is not implemented, minority participants would implement 105 million cash-outs, depleting $500 billion from the retirement system over the 40-year period.

Figure 1- Auto Portability Simulation Results, Minorities

The 40-year scenario we used for our APS is significant because last year (2018) marked the 40th anniversary of the advent of the 401(k). As plan sponsors and those who service them look ahead to the next 40 years, it is important that every effort is made to give participants—and especially minorities, women, and other groups of participants who have high cash-out rates—a fighting chance to preserve their 401(k) savings in the retirement system. The best, and easiest, way for sponsors and their service providers to do so is to adopt auto portability.