Cashout leakage, a long-standing problem in America’s defined contribution system, is a silent crisis that unnecessarily robs millions of Americans of a comfortable, timely or secure retirement. Plagued by misunderstanding and neglect, it’s vitally important to understand the problem and to take decisive action to curb it.

Cashout leakage, a long-standing problem in America’s defined contribution system, is a silent crisis that unnecessarily robs millions of Americans of a comfortable, timely or secure retirement. Plagued by misunderstanding and neglect, it’s vitally important to understand the problem and to take decisive action to curb it.

The second of a five-part series, this article addresses the demographics of cashout leakage.

Who’s Cashing Out?

With approximately 14.8 million 401(k) participants changing jobs each year and 4.7 million (31%) of them cashing out in the first year following separation, cashout leakage affects a broad swath of Americans. Understanding the demographics of cashout leakage can help inform retirement savings public policy by more effectively identifying segments of the population who stand to derive the most benefit from solutions that address the problem.

Examining the relevant industry research, it’s clear that specific demographic segments – including job-changing participants who have lower account balances and/or lower incomes, are younger, are women or are minorities – experience higher levels of cashout leakage than the general population.

Two sources of data help bring the demographics of cashout leakage into focus:

- Studies conducted by large defined contribution recordkeepers (Fidelity, Vanguard and Alight) have examined broad patterns of cashout leakage behavior by account balance, income level and age.

- Other, more specialized studies, such as those conducted by Ariel Investments/Aon Hewitt and by Vanguard, have further explored the impact of cashout leakage by gender, race and ethnicity.

Account Balance, Income and Age

The relationship between 401(k) leakage and account balances, income and age is clear and consistent over time.

As account balances, incomes and age rise, cashout leakage tends to fall:

- Across all recordkeeper studies, for balances less than $1,000, cashout rates are as high as 80%, then gradually fall as balances increase, first dipping below 30% as balances rise above the $15,000 to $25,000 range.

- According to Fidelity, participants whose compensation was below $20,000 experienced cashout rates of 50%, falling to 36% as income rose to $50,000, and finally, to 13% as income exceeded $100,000.

- According to a 2019 Alight study, younger participants are much more likely than older participants to cash out. In a longitudinal analysis covering the period 2008-2017, Alight noted that 51% of participants in their 20s chose to cash out, compared to 43% in their 30s, 41% in their 40s, and 32% in their 50s.

Gender, Race and Ethnicity

When it comes to gender, race and ethnicity, research reveals that cashout leakage exacts a higher toll on both women and minorities.

Gender:

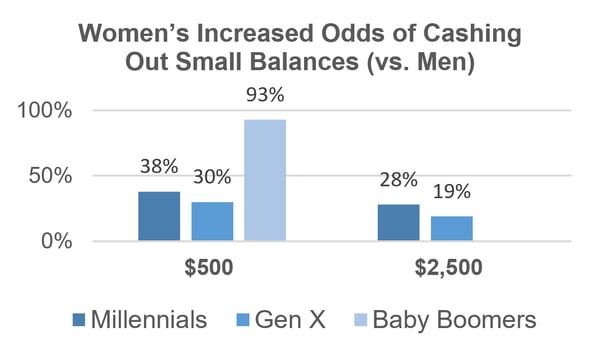

A 2015 survey by Boston Research Technologies revealed that, at sub-$5,000 levels, women of all ages tended to cash out at much higher-levels than their male counterparts, as indicated in the graph below.

Women’s Odds of Cashing Out Small Balances

Source: Actionable Insights for America’s Mobile Work Force, Boston Research Technologies (2015)

On a somewhat more promising note for women, a 2011 study by Aon Hewitt indicated that women – when plan balances rose to between $30,000 and $49,999 preserved their retirement savings at a 36% rate versus 31% of men – effectively “flipping the script” on cashout leakage as their account balances increased.

Race & Ethnicity:

While cashout rates are high across all racial and ethnic groups, African-Americans and Hispanics experience significantly higher cashout out rates than other groups.

In 2012, a study by Ariel/Aon Hewitt found that:

- As a group, African-Americans cash out 63% of the time, and are 61.5% more-likely to cash-out than their white counterparts. At every income and account balance levels, cash-out rates are higher for African-Americans.

- A similar dynamic exists for Hispanic Americans, who cash out 57% of the time, and are 46.2% more-likely to cash-out.

- White Americans, while faring better than African-Americans or Hispanics, still cashed out their balances, on average, 39% of the time upon termination.

Implications for Public Policy

The demographics of cashout leakage are clear, and solutions that effectively address the problem of 401(k) cashout leakage, such as auto portability, will have a broad impact across a diverse segment of America’s population, but will disproportionately benefit those participant segments that have lower incomes, are younger, are women or are minorities.