401(k) plan sponsors know all too well that sunlight – coming in the form of transparent fees and disclosures – is vital to fulfilling their fiduciary duty to act in the best interest of their participants.

401(k) plan sponsors know all too well that sunlight – coming in the form of transparent fees and disclosures – is vital to fulfilling their fiduciary duty to act in the best interest of their participants.

Nowhere is the application of sunlight more urgent than upon the dark corners of safe harbor IRAs, the destination for millions of small-balance 401(k) savers routinely forced out of their plan. It’s there, where no ERISA protections follow, that some former participants may find that safe harbor IRAs aren’t always safe, and they’re subjected to outcomes far worse than the well-documented problem of cashout leakage.

Why Sunlight is Crucial

Safe harbor IRAs exist due to the success of 401(k) plans, combined with the propensity of America’s mobile workforce to change jobs. Together, they foster a small-account problem that the automatic rollover feature was intended to resolve by establishing safe harbor IRAs, where former participants’ savings would be preserved and could even grow.

While safe harbor IRAs have helped plan sponsors mitigate a portion of their cost and risk, they’ve failed miserably for participants. Cashout rates are sky high, and 99% of the survivors earn near-zero money market returns, never changing their default investment fund.

In October 2020, EBRI research identified safe harbor IRAs as the culprit driving a small-balance IRA explosion, where approximately 77%, or 8.1 million, were likely safe harbor IRAs. It’s within this massive “landfill” of safe harbor IRAs that some providers have learned to generate big profits – big enough to pay fees to third parties, including recordkeepers, TPAs, technology outfits, advisors and occasionally, even plan sponsors. To maximize their profits and pay third parties, these providers hammer former participants with excessive fees, pricy and sub-optimal investments and even erect barriers to exit.

While not illegal, the sheer number of fees that former participants can face should offend the sensibilities of fair-minded people in the same manner as credit card late fees, payday loans and other excessive fee financial practices.

For example, a search of the internet reveals actual safe harbor IRA fees that include:

- Initial setup fees, of up to 20% of the initial balance

- Annual maintenance fees, paid up front

- Account closure fees

- Search fees, if a former participant is deemed missing or deceased (over $100 per search)

- Paper statement fees (up to $15 per mailing)

- Escheatment fees ($125 per account)

- Residual dividend distribution fees

- Check reissuance fees

- Roth conversion fees

- Federal Thrift Savings Plan rollover fees

…and more.

While the provider’s profits are impressive, the costs to former participants are shocking.

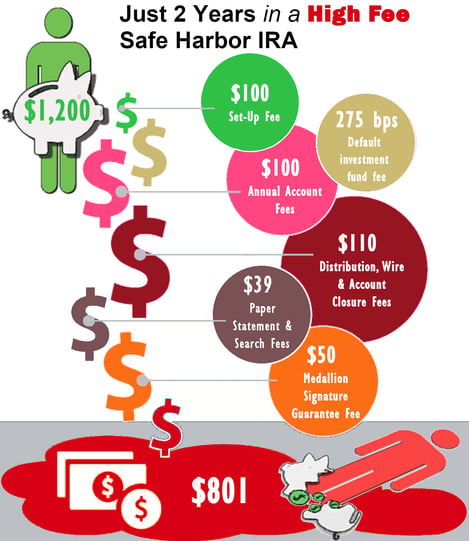

In the hypothetical illustration below, which applies a subset of the above fees, a 25-year old former participant with a $1,200 401(k) plan balance would retain only $801 in their account after spending just two years in a safe harbor IRA. That’s almost $400 in fees!

Figure: Two Years in a High Fee Safe Harbor IRA

If our hypothetical former participant cashed out, they would net around $550, after taxes and penalties. By contrast, had the same individual moved their 401(k) savings forward, that $1,200 balance would be worth around $12,000 at retirement.

To add insult to injury, liberating what remains of their funds can become a costly hassle, as some providers require that they supply a medallion signature guarantee, which can cost around $50, assuming they can get one. Finally, should the truly motivated get their distribution and attempt to roll it in to their new plan, they’ll have to navigate a DIY roll-in process on their own.

For safe harbor IRA accountholders who leave their savings unattended, the layered fees remorselessly drain their balances until the bitter end. That end arrives when balances dip below the level of their provider’s final applicable fee, coming in the form of an account closing fee or an escheatment fee, which reduces the balance to $0 and closes out the account.

What Plan Sponsors Can Do

Plan sponsors who adopt automatic rollover provisions have a fiduciary responsibility to act in the best interest of their participants, and that includes obtaining a complete & accurate understanding of all relevant service fees, third-party arrangements and other factors that can materially affect their participants’ retirement benefits.

Unfortunately, many plan sponsors simply accept the default automatic rollover solution bundled with their primary provider. If, and when they perform due diligence, it can be cursory, or focused solely on specific aspects of the automatic rollover service (ex. – annual fees and default investment options), while ignoring other important account fees, external arrangements or obstacles.

To shine light on safe harbor IRA fees, here's what plan sponsors need to ask of their safe harbor IRA service provider:

1. Request, in writing, a complete list of all participant fees.

2. Closely examine default investment fees and provisions, paying specific attention to:

- Fee amounts and structure

- Parties earning fees and their respective shares

- Fund lock-up provisions, exit fees or other potential liquidity issues

3. Request, in writing, all third-party fee sharing arrangements, paid in advance or following the establishment of safe harbor IRAs.

4. Identify any barriers to exiting the safe harbor IRA (ex. – signature guarantees).

5. Identify the level of assistance offered to former participants for consolidation, if any, including rollovers and plan roll-ins.

6. Request historical metrics, with supporting figures, for:

- Percent cashout leakage, including the cashouts that occur during the initial participant notification period

- Median account duration

- Number of consolidations assisted

By asking the right questions, 401(k) plan sponsors can ensure that their former participants won’t face excessive safe harbor IRA fees, pricy investments and barriers to exit. In so doing, they’ll not only brighten the retirement prospects for their participants, they’ll protect themselves by properly performing their fiduciary duty, and will help ensure that safe harbor IRAs live up to their original, intended purpose.