In this five-part series, I identify five key reasons why an auto portability program serves the best interests of plan participants.

In this five-part series, I identify five key reasons why an auto portability program serves the best interests of plan participants. Previously:

- In Part 1, I examined the dramatically improved participant outcomes that will result from a program of auto portability.

- In Part 2, I described how auto portability, by enhancing and extending automatic rollover programs, represents an enhanced standard of participant care.

In Part 3, I present evidence that the adoption of auto portability could lead to a reduction in plan expenses.

Linking Auto Portability to Plan Efficiency, Lower Plan Expenses

Auto portability is the routine, standardized, and automated movement of a retirement plan participant’s 401(k) savings account from their former employer’s plan to an active account in their current employer’s plan.

The U.S. Department of Labor (DOL), in their publication Meeting Your Fiduciary Responsibilities, identifies “paying only reasonable plan expenses” as one of five key fiduciary responsibilities. Auto portability, by preserving participants’ retirement wealth, not only improves participant outcomes, but also moves the needle on key plan metrics, which in turn can drive a more efficient, lower-cost plan.

Auto portability lowers plan costs in two fundamental ways:

- Reducing small-balance accounts

- Increasing plan assets

To demonstrate how auto portability can lower plan costs, we would ideally observe the cumulative behaviors and outcomes for separated participants with less than $5,000 over time – both with and without auto portability – and compare the differences at a plan level. While that’s not practical in the real world, the Auto Portability Simulation (APS) model provides us with a tool to make those comparisons.

The APS is a discrete event simulation that can model the behavior of millions of small-balance, job-changing 401(k) plan participants over a generation. For this analysis, the APS was re-configured to model a hypothetical plan with 10,000 active participants and to compare the results under two scenarios: 1) no auto portability and 2) auto portability.

In both scenarios, our hypothetical plan has:

- 10,000 active, contributing participants

- $1.03 billion in assets, based on an average balance of $103,000

- Plan provisions that allow rollover contributions, or “roll-ins”

- Participant turnover and levels of small-balance accounts consistent with averages from the EBRI/ICI 401(k) Database

- 34,067 job-changing participants with balances less than $5,000, over 40 years

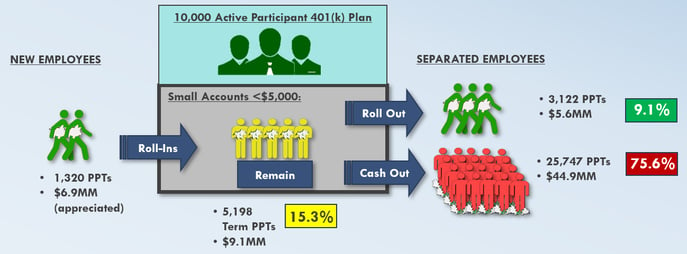

- For our hypothetical plan, under the “no auto portability” scenario (Figure 1), the model yields:

- A modest number of new participants (1,320) rolling in small balances from former plans

- 9.1%, or 3,122 participants, rolling $5.6 million in retirement savings out of the plan, and into other employer plans or IRAs

- 75.6%, or 25,747 participants, cashing out completely

- 15.3%, or 5,198 participants, electing to remain in the plan, leaving behind $9.1 million in savings

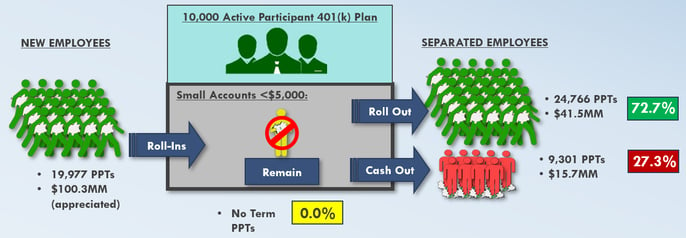

In the “auto portability” scenario (Figure 2), the plan will experience:

- A significant number of new participants (19,977) rolling in small balances from prior plans

- No small balance terminated participants remaining in the plan

- 27.3%, or 9,301 participants, cashing out completely

- 72.7%, or 24,766 participants, rolling $41.5 million in retirement savings out of the plan, and into another employer plan or IRA

Reducing Small-Balance Accounts

In the “no auto portability” scenario, 5,198 terminated participants with small balances leave their savings behind in the plan. As this population relocates, reaches retirement ages, and occasionally, dies – these “stranded” small accounts can cause major headaches for the plan, including returned mailings, uncashed distribution checks, missing participant search costs, and in some cases, plan audits – all of which can drive significantly higher plan expenses.

By contrast, in the “auto portability” scenario, the plan will have no small accounts left behind by former employees and, for small accounts, will not incur the administrative burdens and expenses associated with missing participants and uncashed checks.

Increasing Plan Assets

Under auto portability, the plan sees a dramatic increase in the number of new participants who roll-in their small balances from prior plans. In our model, the appreciated value of these small-balance roll-ins exceeds $100.3 million, an amount that could eventually represent 10% of total plan assets.

This increase in plan assets could make an important contribution to lowering plan expenses.

According to the Deloitte Consulting study Inside the Structure of Defined Contribution/401(k) Plan Fees, “a 1% increase in the average account balance is associated with a 0.22 basis point lower ‘all-in’ fee.”

Combining the results of the APS with the Deloitte Consulting study would yield a 2.2 basis point lower all-in fee, equating to cumulative plan savings of $2.26 million, over the duration of the simulation.

Key Takeaways

- Auto portability, by enabling the consolidation of small account balances – both into and out of plans – dramatically improves retirement outcomes for participants.

- Auto portability creates more-efficient and cost-effective plans, which serve to lower plan costs and further benefit plan participants.