Have you ever received a letter with the notice “Time Sensitive Material! Open Immediately!” boldly splashed across the outside of the envelope, only to sigh with disappointment with what’s on the inside? While the disappointment of false advertising so often seems to be the case with “junk mail,” the warning turns out to be true when we examine the behaviors of retirement plan participants who have recently changed jobs.

Have you ever received a letter with the notice “Time Sensitive Material! Open Immediately!” boldly splashed across the outside of the envelope, only to sigh with disappointment with what’s on the inside? While the disappointment of false advertising so often seems to be the case with “junk mail,” the warning turns out to be true when we examine the behaviors of retirement plan participants who have recently changed jobs.

In 2008, Retirement Clearinghouse began collecting data on participants’ distribution decisions for a large hospital services company’s plan, with more than 230,000 employees and as many as 45,000 participants who changed jobs each year. In every instance, we recorded both the date of termination and the date that the participant made their distribution decision, so that we could accurately report the elapsed time between those dates. We continued to collect the data over the ensuing eight years, an accumulation of more than 300,000 individual decisions that offers actionable insight into participant behaviors at the time of a job change.

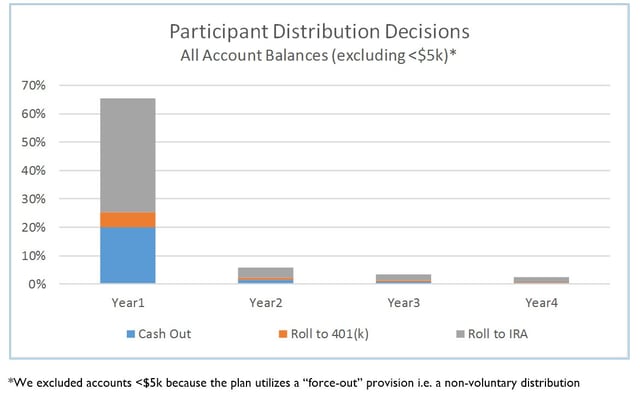

As the headline suggests, one key finding from the data is that a significant majority (65%) of participants will make their distribution decision within the first 365 days of their termination from their former employer (illustrated in the chart below). In subsequent periods, the percentage of participants making distribution decisions drops precipitously, to less than 6% in Year 2, 3.5% in Year 3 and 2.4% in Year 4.

Most of us have gone through one or more job changes in our careers and can appreciate that it is often a time of significant change that is accompanied by high stress—not necessarily the best conditions in which to be making important, long-term decisions about our retirement savings. In his August 2016 testimony to the ERISA Advisory Council, Boston Research Technologies CEO Warren Cormier corroborated that view: before the time of their job change, only 4% of responded that they intended to cash out their retirement savings when they changed jobs. But as shown in the chart above, when faced with the actual decision, 20% made the decision to take the cash, paying taxes and penalties in the process, and doing irreparable damage to their long-term retirement prospects. In his testimony, Cormier also noted that 50% of those participants subsequently regretted their cash-out decision.

The implication for plan sponsors and their service providers is pretty straightforward: participants need to have portability services available to help them make good decisions at the time of a job change, and the key success measure for portability services is the preservation of participants’ retirement savings.

Not a Trivial Problem

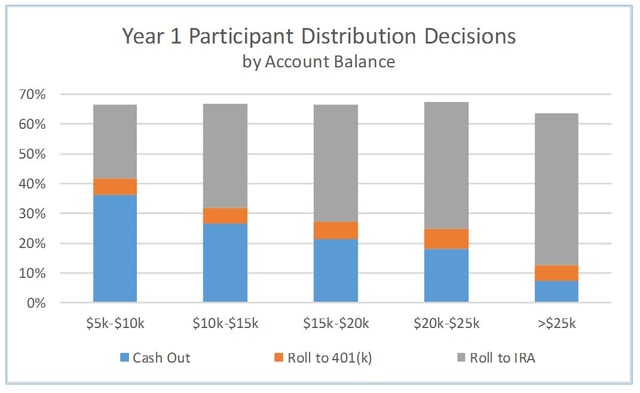

When we segmented the data by account balance, we confirmed another key finding, one that corroborated our experience over a decade of providing phone-based portability services to small accountholders, which we defined as participants with balances of less than $20,000) - small accountholders are cashing out at alarming rates, particularly in the first year after a job change, as illustrated in the chart below.

Even after we excluded accounts with less than $5,000, accounts with less than $20,000 represented 49% of all the participants we serviced. And lest we think that these small account cash-outs don’t matter, the Auto Portability Simulation we developed in cooperation with Dr. Ricki Ingalls of Texas State University found that, in a scenario where cash-outs are reduced by auto portability, for all small accountholders, more than $1.8 trillion would be added to Americans’ retirement savings over the coming generation.

In order to reduce cash-outs as well as the number of small, stranded accounts in their plans, sponsors and record-keepers can offer services that facilitate plan-to-plan portability, including auto portability (the seamless, automatic transfer of retirement savings balances of under $5,000 between plans at the point of job-change). When they do so, either by themselves or with the assistance of an independent roll-in service provider, they are improving the health of their plans and also fulfilling their fiduciary responsibility to help participants make decisions that are in their best interest.

Sponsors and record-keepers can do their part by offering portability services that make it easy for participants, coming and going, to keep their savings invested in the U.S. retirement system during the first year after they switch jobs.